July has opened with the international freight market under pressure from several directions at once: container rates climbing sharply, carriers layering fresh surcharges onto key trades, shipping corridors that remain technically open but commercially fragile, and shifting US trade policy adding further uncertainty. For Australian and New Zealand importers, exporters and freight forwarders, the question is no longer simply whether cargo can move. It is moving. The harder question is whether it can move with enough price certainty, schedule reliability and contractual clarity to support confident business decisions.

This month’s freight market update draws on the latest data from the Freight & Trade Alliance and the Australian Peak Shippers Association, together with reporting from Drewry, the OECD, UNCTAD, the WTO, Sea-Intelligence and other leading industry sources, to give Magellan clients and partners a clear, practical picture of what has changed and what it means for their supply chains.

TL;DR – Global Freight Market Update July 2026

- Global ocean spot rates surged again. Drewry’s World Container Index reached its highest level in over 18 months, now around 40% above the same period last year and close to 50% above late-May levels.

- Carriers including COSCO, MSC, ONE, Hapag-Lloyd, GSL, ZIM and ANL layered rate restorations, peak season surcharges or general rate increases onto the China-Australia trade from 1 July.

- The OECD trimmed its world trade growth forecast to 3.1% for 2026, down from 5.0% in 2025, and reports ocean freight rates sitting around 45% above pre-conflict levels.

- The Strait of Hormuz remains a substantial risk despite a fragile ceasefire, with vessel transits still a fraction of pre-conflict volumes. Exposure for Australia and New Zealand is largely indirect, through fuel and war-risk premiums.

- Global schedule reliability improved to 64.7% in May, its best of 2026, yet the average delay for late vessels lengthened to 5.52 days, nearly a full day more than a year ago.

- Port congestion reached its highest level since 2022, with close to 11% of the global containership fleet waiting at anchorage, concentrated at Singapore, Shanghai and Ningbo.

- Air cargo rates stayed elevated, around 30% above pre-conflict levels, even as Gulf capacity returns.

Freight Market Update: Middle East Disruption

The Strait of Hormuz remains a live commercial risk despite a memorandum of understanding signed by the United States and Iran in mid-June, aimed at ending military operations and reopening the Strait for a 60-day negotiation period. The agreement was non-binding and left key operational questions, including control of shipping lanes and vessel clearance arrangements, unresolved. By late June, the situation had deteriorated again, with renewed attacks on commercial shipping and Iran asserting tighter control over transit, prompting the International Maritime Organization to temporarily pause its Strait of Hormuz evacuation operation following an attack on a vessel in the Gulf of Oman.

What AU/NZ Shippers Need to Know

The Joint Maritime Information Center currently rates the Strait of Hormuz as a substantial threat, the highest rating of any monitored corridor in the region, while surrounding waters sit at moderate. Vessel transits have recovered from the lows recorded earlier in the conflict but remain a fraction of pre-conflict daily volumes. For Australian and New Zealand shippers, exposure is largely indirect, but higher bunker and jet fuel costs, war-risk premiums and altered carrier routings continue to filter through to freight rates and transit times. Separately, the UAE has announced plans to reduce its reliance on the Strait to zero over time, investing in eastern seaboard ports and pipeline capacity outside the chokepoint, a clear signal of how seriously the region is treating the risk.

Red Sea Update

The Red Sea corridor is calmer but has not returned to normal. As at 30 June, no attacks on merchant shipping had been reported in the southern Red Sea, Bab el-Mandeb, northern Red Sea or Suez Canal over the preceding two days, and the threat level is assessed as moderate. Vessel traffic through Bab el-Mandeb remains below pre-2023 levels. Maersk has resumed selected Suez Canal transits and CMA CGM has expanded its use of the route, but the large majority of container services continue to divert via the Cape of Good Hope, adding significant time and cost to Asia-Europe trades.

What This Means For You:

Even where a route is technically open, that is not the same as it being commercially reliable. Continue to build a buffer into transit-time expectations for Middle East-linked trades, review your exposure to war risk and emergency surcharges, and speak to your dedicated account manager about alternative routing options if your supply chain depends on precise delivery timing.

Freight Market Update: Rates and Services

Global Ocean Rates

Global spot rates accelerated sharply through June, with the Drewry World Container Index climbing week-on-week to its highest level in more than 18 months, now sitting close to 40% above the same period last year and nearly 50% above levels recorded at the end of May. The rally has been driven by strong gains on both the Transpacific and Asia-Europe lanes, with a double-digit weekly increase on the Shanghai-Los Angeles route and solid gains from Shanghai to New York, as importers continue to frontload cargo ahead of anticipated US tariff changes and a bunker fuel adjustment that took effect from 1 July. Intra-Asia rates eased slightly week-on-week but remain up materially month-on-month and more than double pre-conflict levels, reflecting longer routings, elevated bunker costs and continued trade diversification into South East Asia.

Australia

For Australian importers, the China-Australia trade remains the primary pressure point, with schedule disruption, port omissions, blank sailings and carrier confidence around July rate restorations combining to push southbound import pricing higher. COSCO, MSC, ONE, Hapag-Lloyd, GSL, ZIM and ANL have all announced rate restorations, peak season surcharges or general rate increases effective from 1 July, layering further cost pressure across both North East Asia and South East Asia origins. Members should treat these as two distinct markets rather than a single Asia-Australia trade, as pricing and capacity behaviour is now diverging by origin region. On the services side, ANL, COSCO and OOCL have announced a new weekly express loop connecting China and Australia from late July, adding capacity into the traditional peak season, while ANL is separately revising its China-PNG-Queensland rotation to remove several direct port calls in favour of transhipment via Hong Kong.

What This Means For You:

With carriers moving in close succession on restorations and surcharges, budget certainty for the September quarter depends on getting ahead of these changes now. Speak to your dedicated account manager about how the layered increases affect your specific trade lane, and ask about contract rate options that offer more predictable pricing than the spot market.

Freight Market Update: Trade Outlook

The OECD’s latest Economic Outlook projects world trade growth moderating from 5.0% in 2025 to 3.1% in 2026 and 2.9% in 2027, with global GDP growth slowing over the same period before a modest recovery. The OECD links ongoing Middle East disruption directly to higher energy, fertiliser and industrial input costs, and confirms that global ocean freight rates remain around 45% above pre-conflict levels, with air freight around 30% higher. The WTO’s Goods Trade Barometer tells a similar story: global merchandise trade is holding above trend, but momentum is easing, with container shipping and international air freight indices both still signalling expansion, driven largely by demand for electronic components linked to AI-related investment.

US Shipping Update

US-bound container demand remains exceptionally strong as importers continue to bring cargo forward in anticipation of tariff changes, pushing Transpacific rates sharply higher and lifting volumes through the Ports of Los Angeles and Long Beach. Trade policy uncertainty has also escalated, with the US administration threatening to impose a substantial tariff on goods from countries that impose a Digital Services Tax. Several established legal pathways for such a measure appear constrained, and immediate implementation looks unlikely, but the pattern is a familiar one: renewed tariff rhetoric is adding uncertainty to global cargo markets well before any measure is confirmed.

What This Means For You:

Frontloading ahead of tariff and policy changes is compounding tight capacity across the Pacific, with flow-on effects for space and equipment availability into Australia and New Zealand. If your supply chain touches the US market, build contingency into your shipping plans now rather than waiting for policy clarity that may take time to arrive.

Global Schedule Reliability

Global schedule reliability improved to 64.7% in May 2026, its best result so far this year and a continuation of the recovery trend since March, although it remains slightly below the same period last year. Maersk led the major carriers, followed by Hapag-Lloyd and MSC, while newer alliance structures, such as the Gemini Cooperation, continued to outperform older groupings by a wide margin. Despite the improvement, the average delay for late vessel arrivals edged higher to 5.52 days, nearly a full day more than the same period last year, showing that when vessels do miss schedule, recovery is taking longer.

Global Port Congestion

Port congestion worsened through June, reaching its highest level since 2022, with close to 11% of the global containership fleet currently waiting at anchorage. Pressure is concentrated at key transhipment and export hubs, particularly Singapore, Shanghai, Ningbo, Qingdao and India’s Nhava Sheva, as cargo frontloading, weather disruption and vessel bunching combine to strain terminal operations. With global reliability improving but congestion still building at major hubs, the risk to Australian and New Zealand supply chains reliant on Singapore and Port Klang transhipment services is expected to persist through the peak season.

What This Means For You:

Improving global reliability does not remove the risk of missed transhipment connections at congested hubs. If your cargo transits Singapore or Port Klang, build additional buffer into your planning through the third quarter and keep your account manager informed of any time-critical shipments.

Freight Market Update: Capacity Management and Blank Sailings

Global

Ocean freight operations are showing signs of stabilisation, with blank sailings across the major East-West trades falling sharply to a cancellation rate of just 3% over the coming five weeks, down significantly from last month. Most remaining disruption is concentrated on the Transpacific eastbound trade, followed by Asia-Europe, while the Transatlantic remains comparatively stable. Gemini Cooperation and MSC continue to stand out for the strongest schedule adherence.

Australia

Australian shipping schedules are also showing less reliance on aggressive capacity controls, with the blank sailing rate falling by close to a third month-on-month, though it remains elevated by international standards. The decline suggests carriers are becoming more confident in underlying demand and operating conditions, even as rate restorations continue to be layered onto the trade.

Fewer blank sailings is a welcome signal, but capacity discipline can shift quickly during peak season. Keep booking lead times realistic and talk to your account manager early if you have volume commitments that depend on consistent sailing frequency.

Freight Market Update: Equipment

Container equipment availability remained a live issue through June, particularly for Australian exporters requiring reefer and specialised units, with shortages compounded by tighter vessel capacity and an earlier-than-usual peak season. Globally, equipment and space pressures were reinforced by strong frontloading activity on China-US trades. The container manufacturing sector also faced further scrutiny, with a class action filed against major manufacturers following earlier US Department of Justice allegations of price-fixing, while Maersk has backed India’s push to build domestic container manufacturing capacity as part of a broader supply chain diversification effort.

What This Means For You:

If your business relies on reefer or other specialised equipment, book well ahead of your required loading date. Talk to your account manager about securing equipment allocation early, particularly for shipments moving through peak season.

Sustainability

Hapag-Lloyd has moved closer to its target of 100% electronic bill of lading usage by 2030, partnering with WiseTech Global to publish eBLs via its Galileo platform, a move that should help expedite cargo release and reduce reliance on printed documentation. Demand for low-carbon shipping options has softened, however, with average willingness to pay for low-carbon shipping falling from 4.5% in 2024 to 3% in 2025, as cargo owners reassess cost and regulatory uncertainty. Early adopters, including several major European retailers, continue to pay a premium for lower-emission fuel solutions, suggesting green freight demand is becoming more selective rather than disappearing.

What This Means For You:

Sustainability commitments do not need to mean paying a premium across your entire supply chain. Speak to your account manager about where digital documentation and lower-emission options make the most commercial sense for your specific trade lanes.

Air Freight Market Update

Global

Worldwide air cargo rates remain well above last year’s levels despite further capacity returning to the Middle East and Gulf markets, with global chargeable weight up materially year-on-year, particularly across Asia-Pacific and Middle East-linked lanes. The recovery of capacity in the Middle East and South Asia following the latest ceasefire has narrowed the regional capacity deficit relative to pre-war levels, but the Gulf recovery remains uneven, and passenger belly-hold capacity is still not fully restored on key routes. IATA has downgraded its 2026 global air cargo growth outlook to reflect these constraints, while still forecasting cargo revenue to rise as the market shifts from volume-led growth to price-led revenue.

Australia and New Zealand

For Australian and New Zealand importers and exporters, the practical impact is that the broader Asia Pacific air freight market continues to be priced as constrained, even where capacity is technically returning. Shippers are continuing to face tight space, longer lead times and elevated costs, particularly for freight moving through major Asian and Gulf hubs, a pattern especially relevant for perishables, pharmaceuticals and time-sensitive manufacturing inputs. Qantas Freight also experienced operational delays at its Sydney facility during June due to increased inbound volumes and equipment issues, though the carrier has advised that equipment faults have now been rectified and additional resources deployed.

What This Means For You:

If your business ships perishables, pharmaceuticals or other time-sensitive freight by air, build longer lead times into your bookings for the remainder of peak season. Speak to your account manager about the most reliable routing options currently available.

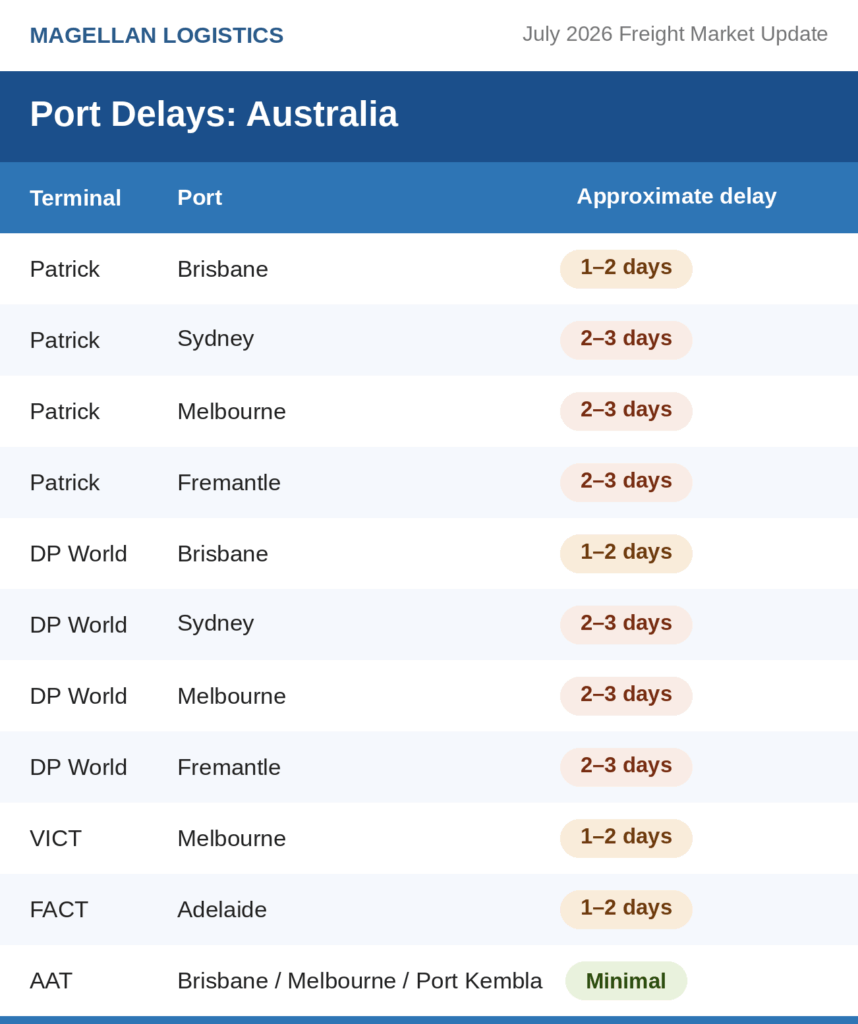

Terminals and Ports

Australia

Australian Border Force cargo reporting data for May shows sea cargo import volumes down slightly year-on-year, while air cargo imports rose strongly, reinforcing air freight’s role as the primary growth driver, and export declarations eased. The 2025 Container Port Performance Index shows encouraging, if mixed, progress for Australian ports. Melbourne recorded the greatest improvement among the major capital city gateways, and Brisbane also moved up significantly, though most Australian ports remain well down the global rankings on vessel time in port, underlining the case for continued investment in berth productivity and landside coordination.

New Zealand

New Zealand’s main container ports continue to experience moderate delays, broadly consistent with the levels reported over recent months.

Notable Infrastructure Developments

Hutchison Ports Sydney has taken delivery of two new quay cranes at its Port Botany terminal, significantly increasing its capacity to handle larger vessels and future-proofing NSW container handling capacity, while Port of Melbourne’s inaugural Trade in Review report confirms the port handled a record volume of container throughput in 2025, reinforcing its position as Australia’s largest container gateway.

What This Means For You:

Terminal delays remain a normal part of peak season operations across most major Australian and New Zealand ports. Build these into your delivery planning and stay in touch with your account manager for the latest terminal-specific advice on your trade lane.

The Bottom Line

July’s freight market update points to conditions that remain functional but increasingly unforgiving. Rates are climbing again, geopolitical risk continues to shape costs and reliability even where routes are technically open, and carriers are moving in close succession on restorations and surcharges. None of this means cargo cannot move. It means the businesses that plan for volatility, rather than being surprised by it, will be the ones that keep their supply chains predictable through the second half of the year.

That is exactly where a dedicated account manager earns their place. Nobody expects you to track every rate restoration, every alliance reshuffle or every shift in geopolitical risk on top of running your own business. Let the experts at Magellan Logistics manage your supply chain so you can focus on what truly matters.

Ready to review your freight strategy for the second half of the year? Speak to an expert today.

Read previous freight market updates and the latest logistics insights at Freight Forwarding News and Insights – Magellan Logistics

About David Thatcher: David, founder of Magellan Logistics, has built a global career in freight forwarding. With international leadership experience and Harvard training, he remains committed to client needs and nurturing his team.

Sources: With thanks to the Freight and Trade Alliance for their freight market update. Figures attributed to Drewry, Sea-Intelligence, WorldACD, UNCTAD, Instant Freight Rates Online – Free Sign up | YQN, and the Australian Bureau of Statistics as reported in the latest FTA/APSA Shipping Report.