The Middle East conflict and shipping disruption has reshuffled the deck for ocean and air freight. What looked like a year of softening container shipping and steady air cargo rates to Australia and improving capacity has given way to surcharge layering, fuel volatility and routing uncertainty. Here’s the latest Australia freight market update for shippers navigating these challenging conditions.

TL;DR: What Australian Shippers Need to Know

- Rates are climbing, not falling. The Drewry World Container Index is up 14.4% since the escalation of the Middle East conflict. Multiple carriers have announced surcharges of US$300–600 per container to Australia, effective April.

- Red Sea transits remain off the table. Maersk, Hapag-Lloyd and CMA CGM are all routing via the Cape of Good Hope again, adding 1–2 weeks to transit times and 20–50% to freight costs.

- Air freight is no longer a clean workaround. Gulf hub capacity is running at 20–75% of normal. Spot rates from the Middle East and South Asia jumped 22% week-on-week in mid-March.

- Fuel is the wildcard. Strikes on energy infrastructure have removed critical production capacity. Fuel availability—not just price—is emerging as a constraint.

- Australia-specific impacts: 11.9% blank sailing rate (up from 9.5%), terminal delays of 1–3 days across major ports, and persistent equipment shortages for refrigerated and standard containers.

- One bright spot: The Australia–EU FTA was finalised on 24 March, with 97.8% of goods exports to enter duty-free.

Bottom line: The soft market many expected in 2026 has evaporated. Flexibility, early booking and close engagement with your freight forwarder are now essential.

Freight Market Update – The Big Picture: A Market That Flipped

Coming into 2026, the outlook was relatively benign. Record newbuild tonnage was hitting the water, carriers were eyeing a return to Red Sea transits, and rates were expected to drift lower. That trajectory lasted about two months.

The escalation of conflict in the Middle East—and specifically the disruption around the Strait of Hormuz—has reversed market conditions with remarkable speed. Carriers have moved from defending rates in a soft market to reasserting pricing discipline through emergency surcharges, tighter capacity management and service adjustments.

The Drewry World Container Index has climbed 14.4% since the conflict intensified, reaching US$2,172 per 40ft container. Intra-Asia spot rates are up 17%. And while Australia isn’t directly on the core conflict lanes, the ripple effects are unmistakable: vessel redeployments, equipment shortages, transhipment bottlenecks and a string of new surcharges have shifted the market firmly back in carriers’ favour.

What this means for you: The softer rate environment many shippers were counting on has evaporated. Budget assumptions made in late 2025 will need to be revisited, and flexibility on routing and timing is now a competitive advantage rather than a nice-to-have.

Container Shipping Rates Australia: Surcharges Stack Up

Carriers aren’t waiting to recover costs. Over the past month, surcharge announcements have come thick and fast, significantly impacting ocean freight rates to Australia:

- MSC is implementing a US$300/TEU rate restoration from North and Southeast Asia to Australia and New Zealand, effective 1 April.

- ANL (CMA CGM Group) is applying a rate restoration of US$300/20′ and US$600/40′ from Asia, the Indian Subcontinent and the Middle East to Australia and New Zealand from 1 April, layered on top of spot and FAK rates.

- ANL is also introducing a GRI effective 16 April of US$350/TEU and US$700/FEU on services linking Asia with PNG, Solomon Islands, Vanuatu, Gladstone, Townsville, Dili, Darwin, Dampier and Port Hedland.

- CMA CGM has published FAK increases from Türkiye, Egypt and Syria to Australia and New Zealand—up to US$500/20′ and US$1,000/40′ from 1 April.

- Maersk implemented an Intermodal Fuel Fee across Australia from mid-March, lifting landside transport costs by approximately 16–17% nationwide. Additional charges take effect: a Late Gate Export fee increase (from A$425 to A$460) effective 1 April, and a new Payer Amendment Fee of US$40 per document effective 1 May.

Shipping Schedule Reliability: Better, But Still Fragile

There’s a brighter spot in the data. Global liner schedule reliability opened 2026 at 62.4%—the strongest monthly result since 2021. Year-on-year, that’s an 11-percentage-point improvement.

Hapag-Lloyd and Maersk led among the major carriers at 72.2% reliability, while the Gemini Cooperation alliance posted close to 90%.

The catch: average delays for late vessels rose to 5.17 days, the highest since February 2025. So, while more ships are arriving on time, those that don’t are arriving later than before.

What this means for you: Reliability is improving at the macro level, but variability remains. Build buffer into critical supply chains and don’t assume schedule stability based on averages alone.

Blank Sailings Australia: Capacity Tightening

Globally, 43 blank sailings have been announced across weeks 13 to 17 from 708 scheduled departures—a 6% cancellation rate. Most are concentrated on the Transpacific eastbound (58%) and Asia–Europe routes (28%).

Australia’s picture is tighter. Nineteen blank sailings from 159 planned departures represent an 11.9% cancellation rate—up from under 9.5% during Lunar New Year. Carriers are deliberately managing capacity, and the elevated cancellation rate suggests ongoing discipline rather than a temporary correction.

What this means for you: Space remains available for now, but carriers are clearly prepared to pull capacity to protect rates. Book early and confirm allocations, particularly for time-sensitive cargo. If you’re managing imports from China or other key Asian markets, planning is critical.

Australia Port Congestion: Pressure Points Shifting

Congestion has spread beyond traditional hotspots. As cargo diverts away from the Persian Gulf, alternative transhipment hubs around the Arabian Sea and Indian Subcontinent are absorbing the strain—including Salalah, Khor Fakkan, Fujairah, Sohar, Mundra and Colombo.

Singapore saw delays peak at 3.5 days before easing later in March. European ports, by contrast, are not currently a primary concern for congestion.

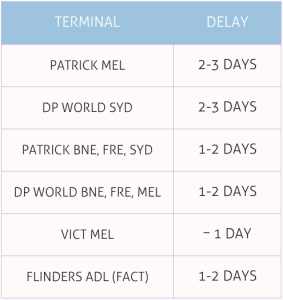

Closer to home, Australian terminal delays remain manageable but present:

New Zealand ports are experiencing 2–3-day delays across Auckland, Tauranga, Napier, and Lyttelton.

What this means for you: Congestion is dynamic and follows the cargo. If your supply chain relies on transhipment through Asia-Pacific hubs, monitor conditions closely and consider contingency routing. A dedicated account manager can help you navigate these shifting bottlenecks.

Air Freight Market Update – Air Cargo Rates Asia to Australia: No Longer a Clean Workaround

Air freight is facing the same pressures as ocean freight. Airspace restrictions and security risks have forced reroutes, increased fuel burn and reduced effective capacity through Middle East hubs.

Global average air rates rose 10% week-on-week in mid-March to US$2.67/kg, with spot rates up 12% to US$3.19/kg. The Middle East and South Asia saw the sharpest movements—spot rates jumped 22% week-on-week to US$4.37/kg, up 58% year-on-year.

Gulf hub operations remain well below normal: Emirates at approximately 75% capacity, Etihad around 50%, flydubai at 33% and Qatar Airways just 20%. With bellyhold capacity through Dubai, Abu Dhabi and Doha central to east–west flows, the knock-on effects are significant.

Jet fuel prices have nearly doubled to around US$197 per barrel. Cathay Pacific lifted fuel surcharges by 34% from 1 April. Forwarders report tighter schedule flexibility, higher spot pricing and more volatile conditions—particularly for time-sensitive, pharmaceutical and perishable cargo.

What this means for you: Air freight is no longer a simple hedge against ocean disruption. Factor in higher costs, reduced reliability and the possibility that air capacity constraints will persist for some time. For urgent shipments and details about air cargo rates to Australia, speak to an expert about the most cost-effective routing options.

Middle East Shipping Disruption: The Fuel Factor

The defining escalation of this crisis has been its impact on energy supply. Strikes on Qatari natural gas infrastructure and the destruction of Iran’s primary crude export facility have removed critical production capacity. Several governments have already implemented fuel rationing.

For freight operators, this translates into higher bunker prices, constrained availability, and rising insurance costs—all of which feed directly into surcharges and rate volatility.

What this means for you: Fuel availability, not just price, is emerging as a constraint. This has implications for both ocean and landside transport, particularly in regions with limited refining capacity.

Red Sea Shipping Delays: Still No Return in Sight

Any hope of a return to normal Suez Canal transits has faded. Maersk, Hapag-Lloyd and CMA CGM briefly signalled a mid-February resumption with naval escort, but by early March, all three were again rerouting via the Cape of Good Hope.

The impact is substantial: freight costs up 20–50%, fuel consumption up around 40% for Cape diversions, and transit times extended by one to two weeks. Even when conditions eventually improve, the return to Suez will trigger months of vessel reshuffling, port congestion and network disruption.

For more background on how the Red Sea crisis developed, see our earlier coverage in the February 2026 freight market update.

Trade Policy: New Architecture, New Investigations

Australia–EU FTA concluded. After eight years, the agreement was finalised on 24 March. The EU is Australia’s largest trading partner without an existing FTA, and Canberra says 97.8% of goods exports will enter duty-free when the deal takes effect. Sectors to watch include agriculture, wine, seafood, advanced manufacturing and critical minerals.

US tariffs continue. The 10% tariffs under Section 122 remain in place until 24 July. The USTR has opened two Section 301 investigations—one covering 16 economies on excess capacity and production, another covering 60 economies on forced labour enforcement. Australia is included in the latter.

What this means for you: The EU deal offers long-term diversification benefits. The US investigations are worth monitoring, particularly for exporters with supply chains touching named economies. Navigating the challenging and uncertain world of trade policy is easier with expert guidance.

Australia Supply Chain News: Domestic Developments

Sydney–Perth rail corridor reopens. The freight corridor is back in service after a five-week closure due to flooding, restoring a critical east–west link. The scale of repairs—over 5,300 hours—underscores how vulnerable inland infrastructure remains to severe weather.

Melbourne rail push. Patrick Terminals is waiving its Exchange Transfer Charge for eligible containers moved by rail to and from Patrick PortRail Melbourne until 2028. Salta is advancing two major intermodal terminals in Dandenong South and Altona. With Victoria’s freight volumes forecast to more than double by 2050, rail-enabled infrastructure is becoming increasingly important.

Equipment shortages persist. Container availability remains tight across multiple lines, particularly for 20GP, 20RF, 20FQ and 40RF units. This is creating ongoing pressure on supply chains for temperature-sensitive and bulk agricultural shipments.

What this means for you: Domestic logistics constraints add another layer of complexity. Early booking and proactive communication with your freight partner can help secure equipment and avoid costly delays.

Sustainable Shipping Australia: Progress on the Ground

Electric towage in Melbourne. Port of Melbourne has signed an MoU with Svitzer, CIP and Plexar Energy to explore Australia’s first fully electric towage operation, including two electric tugs and supporting charging infrastructure.

Ammonia bunkering in the Pilbara. Pilbara Ports and Yara Pilbara are progressing a low-carbon ammonia bunkering hub at Dampier and Port Hedland, supporting the goal of having all bulk export vessels departing the region powered by low-carbon fuels by 2050.

What this means for you: Decarbonisation is moving from ambition to practical planning. For shippers with sustainability commitments, these developments signal growing options for lower-emission freight in Australian supply chains.

Key Takeaways for Australian Shippers

- Revisit cost assumptions. Surcharges are stacking up faster than many anticipated. If your 2026 freight budget was based on late-2025 expectations, it’s time for a reset.

- Build in flexibility. Routing, timing and mode selection all matter more in a volatile market. The shippers best positioned are those with contingency options.

- Stay close to your freight forwarder. Carrier negotiations, surcharge tracking and rerouting decisions are moving quickly. Expert guidance is more valuable than ever.

- Watch fuel, not just rates. Fuel availability and price are now primary drivers of cost volatility across ocean, air and landside transport.

- Plan for the long haul. The Middle East disruption, Red Sea diversions and US trade policy uncertainty are not short-term blips. They’re shaping the operating environment for the foreseeable future.

Ready to Optimise Your Supply Chain?

Navigating the challenging and uncertain world of freight and logistics requires a partner who understands both the global forces at play and the specific needs of Australian and New Zealand businesses. With 28 years of experience, 270+ locations worldwide and dedicated account managers for every client, Magellan Logistics is here to help you manage complexity and avoid costly mistakes.

Speak to an Expert about how these developments affect your supply chain.

Related Reading

About David Thatcher: David, founder of Magellan Logistics, has built a global career in freight forwarding. With international leadership experience and Harvard training, he remains committed to client needs and nurturing his team.

This Australia freight market update is published regularly by Magellan Logistics. With thanks to the Freight and Trade Alliance for their freight market update.

Subscribe to receive the latest shipping market intelligence direct to your inbox.