Welcome to the Magellan Logistics freight market update for June 2026. As we move into the second half of the year, the market is being shaped by three forces at once: rising ocean rates, an earlier-than-usual peak season, and continued instability around the Strait of Hormuz. For importers and exporters across Australia and New Zealand, the headline is that cargo is still moving, but at a higher cost and with less certainty than it was even a month ago.

This freight market update brings together the latest data from Drewry, Sea-Intelligence, WorldACD, the Australian Bureau of Statistics and the Freight and Trade Alliance, and translates it into what it means for your business. As always, our aim is to help you plan with confidence and avoid costly surprises.

TL;DR – Global Freight Market Update June 2026

- Ocean spot rates rose for a fourth straight week. Drewry’s World Container Index reached US$2,800 per 40ft container, 23% higher than a year ago.

- Spot rates from China to Australia have climbed by a cumulative 68% since mid-March, with the Shanghai-to-Sydney indicator at US$2,634 per FEU.

- The Strait of Hormuz remains a critical maritime risk. Uncertainty, not closure, is the real commercial threat.

- Australian blank sailings reached 13.9% of planned departures, well above the global average of around 7%.

- Air cargo rates held firm at US$3.23 per kilogram, still 35% higher year on year, with Gulf capacity around 32% below pre-conflict levels.

- Container shortages persist in Australia, particularly for reefer and specialised equipment.

Freight Market Update: Middle East Disruption

Tensions across the Middle East continue to weigh heavily on both ocean and air cargo markets, and a recent escalation has again exposed how fragile the trade routes connected to the Strait of Hormuz remain. It is tempting to treat the Strait as a simple open-or-closed question. In practice, the real commercial issue is uncertainty. Vessels may delay transit, wait for security guidance, adjust routing, or sail under higher war risk premiums and tighter insurance conditions.

For cargo owners, the exposure is not only whether goods can move, but also whether they can move with sufficient timing certainty to support production schedules, inland logistics, and contractual delivery dates. Even where a vessel can technically transit, ships may loiter, defer entry or divert mid voyage while waiting for updated advice. A single missed berthing window can flow through to terminal planning, road and rail allocations, inventory availability and factory schedules. In some sectors, the cost of late cargo can exceed the cargo’s value.

What Australian and New Zealand Shippers Need to Know

The broader geopolitical setting remains volatile, with the United States and Iran reportedly exchanging further strikes even as negotiations continue. For Australian and New Zealand shippers, the exposure is largely indirect but still significant. Higher bunker and jet fuel costs, disrupted Gulf air cargo capacity, altered carrier routings and war risk premiums all have the potential to flow through to freight rates, transit times and reliability.

Operational warnings have also become more serious. A United States advisory has cautioned that vessels near Hormuz that ignore lawful orders, or are seen supporting mine laying, may be treated as threats. Reports that components of an Iranian anti-ship missile were linked to damage on a container vessel underline that merchant shipping is now operating within a genuine military risk environment. The overall maritime risk level for the Arabian Gulf and Strait of Hormuz is currently assessed as critical.

Red Sea Update

The wider conflict continues to influence routing, fuel consumption and carrier cost bases. Red Sea diversions have already reshaped network economics by routing vessels around the Cape of Good Hope, thereby lengthening transit times and reducing effective capacity. Any escalation around Hormuz compounds that strain, leaving carriers managing disruption at two critical maritime pressure points rather than one. Longer voyages are also placing pressure on bunkering, with additional refuelling stops absorbing vessel capacity and reducing schedule resilience across global networks.

What This Means For You:

If your supply chain relies on precise timing of inputs, build extra lead time into your June and July planning and talk to us early about contingency routing. We monitor these developments daily and can help you weigh the cost of holding buffer stock against the risk of late cargo. Speak to an expert if you would like to review your exposure

Rates and Services

Global Ocean Rates

Ocean spot rates extended their run for a fourth consecutive week. Drewry’s World Container Index rose 3% to US$2,800 per 40ft container in late May, 23% higher than a year ago and around 26% higher than the previous month. On the Asia-to-Europe trade, early peak-season demand pushed Shanghai-to-Rotterdam rates up 3% to US$2,861 per 40 ft container and Shanghai-to-Genoa rates up 4% to US$4,253 per 40ft container. CMA CGM has announced new FAK rates from 1 June of around US$4,700 for Asia-to-Europe and US$5,500 to US$5,700 for Asia-to-Mediterranean lanes.

Within Asia, Drewry’s Intra Asia Container Index rose 5% to US$1,008 per 40ft container and is now up almost 10% month on month, driven by higher bunker costs, reduced capacity and firm demand. Carriers are tightening supply through blank sailings and rate restoration programmes, and the broad expectation is for further upward pressure in the coming weeks.

Australia

Closer to home, the pressure is sharper. Mean spot rates between China and Australia have risen a cumulative 68% since mid March, with the Shanghai to Sydney indicator reaching US$2,634 per FEU after a further 9% weekly lift. This increase appears to be driven more by schedule disruptions, port skipping, and carrier confidence in further rate rises than by strong volume growth, which points to a difficult June for importers.

Several carriers have layered on rate restorations from June. GSL and ZIM each announced a US$300 per TEU restoration for dry and reefer cargo from North East and South East Asia to Australia, effective 15 June. COSCO confirmed restorations of US$300 per TEU and US$600 per FEU from 1 June, and MSC announced a US$300 per TEU southbound restoration with a matching peak season surcharge. By contrast, trade between South East Asia and Australia has remained comparatively flat through 2026, a reminder that North East Asia and South East Asia pricing should be treated separately rather than as a single Asia-to-Australia market.

On services, Maersk will launch its Qilin China-to-Australia service from 24 July, offering a Shanghai-to-Sydney-to-Melbourne rotation with weekly departures, while MSC has announced a significant revision to its Oceania network. ANL also confirmed a leadership change, with Esra Bora succeeding Shane Walden as Managing Director from 1 June.

What This Means For You:

For procurement teams, now is the moment to test these restorations and surcharges against your agreed contract terms and update your landed cost estimates before locking in June shipments. We can help you compare carrier options, confirm which increases genuinely apply to your cargo, and protect your margins. Request a rate review, and let’s start a conversation.

Trade Outlook

Global trade remains resilient but increasingly fragile, with growth driven more by price than by volume. According to UNCTAD, the shock from a disruption in the Strait of Hormuz is expected to slow global merchandise trade growth from an estimated 4.7% in 2025 to a forecast range of around 1.5% to 2.5% in 2026. Higher fuel costs, security risks and schedule disruption are all being absorbed into freight rates and surcharges, so headline trade figures should not be mistaken for easier trading conditions.

In Australia, the Australian Bureau of Statistics reported that the economy grew 0.3% in the March quarter and 2.5% over the year, with commentary pointing to slow growth, higher oil prices and cost-of-living pressure. For freight, softer household demand can reduce import volumes, while higher fuel and finance costs raise operating expenses. Some manufacturers have benefited from precautionary stock building, but this is likely temporary. A short-term cargo pulse driven by buffer rebuilding can lift freight activity without signalling sustainable demand.

US Shipping Update

Australian exporters should keep a close eye on a United States tariff proposal. The United States Trade Representative has proposed new Section 301 tariffs covering around 60 economies, with Australia included in a higher band of up to 12.5%. The measures have not yet been implemented and remain subject to consultation, with submissions closing in early July. This is part of a broad, globally applied policy rather than a dispute targeted at Australia, but if implemented, it would add a new cost and compliance layer for goods entering the United States.

What This Means For You:

If you export to the United States, it is worth modelling the impact of a potential 12.5% tariff now and reviewing your supply chain documentation and evidence of labour standards. Our customs and compliance experts can help you prepare. Speak to an expert to understand your options.

Global Schedule Reliability

There is some better news on reliability. Sea-Intelligence reported that global schedule reliability improved again in April to 62.4%, the highest level so far in 2026 and four percentage points better than a year earlier. Maersk led the major carriers at 76.1%, closely followed by Hapag-Lloyd at 75.1%, while Wan Hai recorded the lowest at 39.6%. Average delays for late vessels also shortened to 5.34 days, although that remains slightly longer than this time last year. Among the alliances, Gemini Cooperation stood out at 85.0%, well ahead of the wider market.

Global Port Congestion

Congestion remains a live concern, with reported waits of up to 15 days at some Singapore and Japanese ports for certain bunker fuel arrangements linked to Hormuz supply constraints. This is a different kind of bottleneck. Even when container terminals are operating normally, limited access to fuel can delay departures and create knock-on effects across the network. Berth waiting times across major Asian hubs ranged from under a day at several Chinese ports to around two days at Melbourne.

What This Means For You:

Improving reliability is welcome, but averages hide wide differences between carriers and alliances. When we book your cargo, we factor in real schedule performance, not just the headline transit time, so your estimated arrival dates are realistic. Let’s start a conversation about building this into your planning.

Capacity Management and Blank Sailings

Global

Carriers are managing capacity tightly to support rates. Across the major East-to-West trades, 47 blank sailings are expected over the next five weeks, a cancellation rate of around 7%. The largest impact falls on the Transpacific eastbound trade, followed by Asia to Europe and the Mediterranean, while the Transatlantic is less affected. At the same time, the market is moving into an earlier-than-usual peak season, with Red Sea diversions, tighter capacity, and cargo frontloading ahead of July fuel surcharge increases all lifting booking activity.

Australia

Australia is feeling this more acutely than most. The blank sailing rate to and from Australia has risen to 13.9% of planned departures, well above the global trend. The persistence of double-digit cancellation levels reflects a deliberate effort by carriers to keep supply closely aligned with current demand, and it means available space can tighten quickly even when underlying booking levels are not especially strong.

What This Means For You:

Double-digit blank sailing rates make space planning unpredictable. The practical defence is to book earlier, keep your forwarder informed of your forward order book, and build flexibility into your schedule. As your dedicated account manager, we work to secure the space you need before it tightens. Speak to an expert about your June and July bookings.

Equipment

Equipment availability remains a challenge for Australian importers and exporters. Container shortages continue across several shipping lines, with demand particularly high for 20ft general purpose, 20ft and 40ft reefer and specialised units. That creates ongoing pressure for temperature-sensitive and bulk agricultural shipments, where the right box at the right time is essential.

The longer-term backdrop is also shifting. The United States Department of Justice has alleged that six Chinese manufacturers, who together account for more than 95% of global container production, restricted output and fixed prices for dry containers between late 2019 and early 2024. New container production reached record highs of 6.61 million TEU in 2021 and 7.85 million TEU in 2024 as demand surged. Equipment cost and availability remain structurally important to the rates you pay.

What This Means For You:

If your cargo depends on reefer or specialised equipment, early booking is essential in the current market. We plan equipment needs well ahead for our clients, so a shortage does not become your problem. Let’s start a conversation about your seasonal requirements.

Sustainability

The industry’s energy transition continues to move from aspiration to practical trials. The first bunkering using a pre-blended ethanol-methanol mix was completed in Rotterdam, while Hapag-Lloyd and Kuehne+Nagel launched a sustainable marine fuel pilot targeting around 3,000 tonnes of carbon dioxide equivalent reductions through the use of waste-based fuel. The first solid wind sails are being installed on an LNG carrier under construction in South Korea, and the Port of Long Beach has offered a US$1 million prize for the first methanol bunkering operation at the port.

For shippers, these developments matter because they signal where lower emission options are emerging. The credibility of any low-carbon shipping claim depends on certification, accounting methodology and transparency over the fuel actually used.

What This Means For You:

If reducing the carbon footprint of your freight is on your agenda, we can help you understand the genuine, verifiable options as they become available. Speak to an expert about sustainable freight choices.

Air Freight Market Update

Global

Air cargo markets have broadly stabilised following the rebound from East Asia’s Golden Week period. Global tonnages were flat but remained around 2% higher year on year, according to WorldACD, supported by shippers managing longer ocean lead times. Rates, however, remain elevated. Average full market rates held at US$3.23 per kilogram, still 35% higher than a year ago, while worldwide spot rates edged up to US$3.75 per kilogram, around 50% higher year on year.

The Gulf remains the key constraint. Capacity to and from the Middle East and South Asia remains around 32% below pre-conflict levels, with Gulf capacity reportedly nearly 48% below earlier levels. Jet fuel prices eased from around US$209 per barrel in early April to about US$162 per barrel in mid-May, reducing the immediate risk of another fuel-driven rate spike, although prices remain around 80% higher year on year. The market has stabilised, but it has not normalised.

Australia and New Zealand

For Australian and New Zealand businesses, air freight remains a valuable option for time-critical cargo, particularly where ocean schedule certainty is under pressure. With Gulf capacity still constrained and rates well above last year, careful planning and access to multiple airline options matter more than ever. New next-generation freighter orders from Asian carriers indicate improved capacity over time, though they will not address immediate constraints.

What This Means For You:

When ocean transit times are uncertain, air freight can protect a critical delivery, but only with the right planning. We offer weekend uplifts, deferred services and multiple airline options to match speed and cost to your needs. Speak to an expert about your urgent shipments.

Terminals and Ports

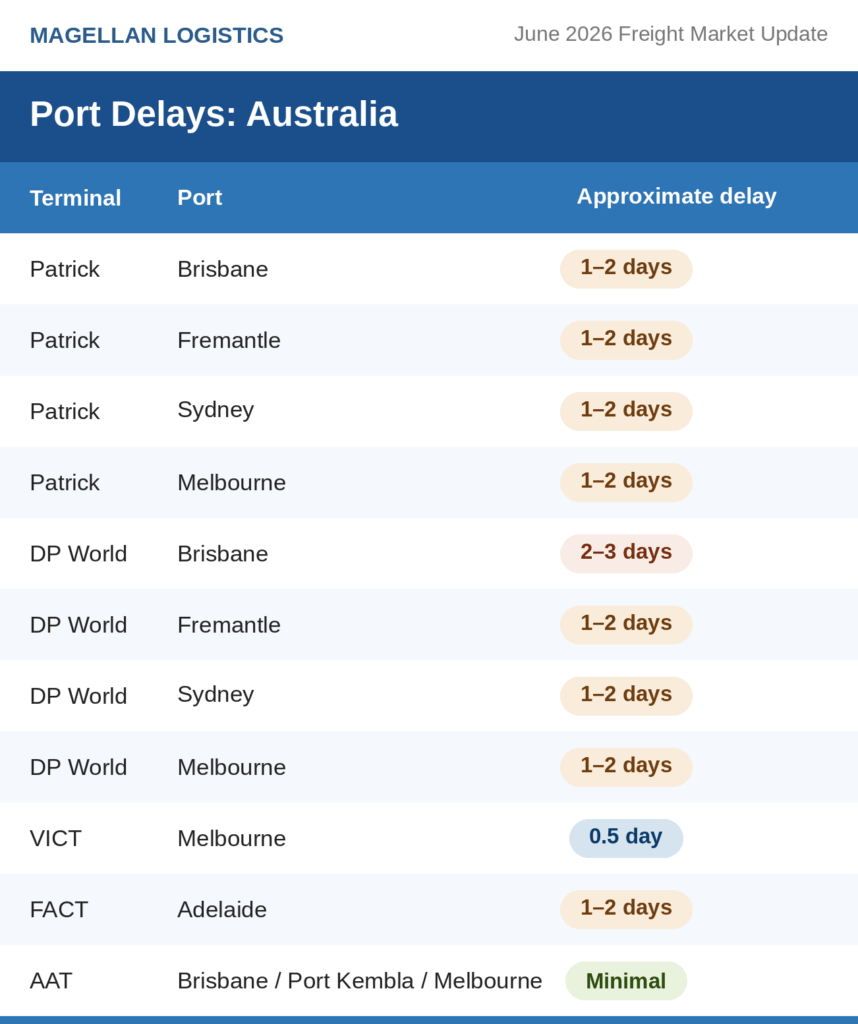

Australia

Australian terminal performance remains mixed. The latest Australian Border Force cargo reporting shows air cargo continuing to drive growth, with reports up around 20% year on year, while sea cargo volumes softened against last year but lifted on the previous month. At the terminals, delays are manageable but present, ranging from minimal at some facilities to two to three days at others.

New Zealand

Across New Zealand, the main container ports continued to run with moderate delays of around two to three days.

Notable Infrastructure Developments

A few infrastructure developments are worth noting. Fremantle Ports has advised that ship and cargo charges will rise 4.6% from 1 July, linked to the Perth Consumer Price Index. Internationally, DP World secured a five-year extension at Laem Chabang in Thailand and is exploring a second terminal in Bangladesh, PSA won the Xiamen terminal expansion bid, and Maersk settled a long-running port dispute in India. Closer to home, Victoria International Container Terminal added new automated container carriers, and Patrick Terminals marked 107 years of operation.

What This Means For You:

Port charge increases and terminal delays both affect your landed cost and delivery timing. We track terminal performance across Australia and New Zealand so we can route your cargo to avoid the worst of the congestion. Speak to an expert about optimising your terminal choices.

The Bottom Line

The freight market entering the second half of 2026 is defined by rising rates, tight capacity and persistent geopolitical risk. Ocean rates are climbing, blank sailings to Australia are running at double-digit levels, equipment is tight, and the Strait of Hormuz continues to inject uncertainty into both sea and air freight. None of this is cause for alarm, but all of it rewards careful planning.

This is exactly the environment where a dedicated freight forwarding partner earns its place. With 28 years of industry experience, customs licensing across Australia and New Zealand, and dedicated account managers who own the problem, Magellan Logistics helps you navigate the complexity so you can focus on running your business.

If you would like to review your freight strategy for the months ahead, we would be glad to help. Speak to an expert, and let’s start a conversation about propelling your business forward.

Read previous freight market updates and the latest logistics insights at Freight Forwarding News and Insights – Magellan Logistics

About David Thatcher: David, founder of Magellan Logistics, has built a global career in freight forwarding. With international leadership experience and Harvard training, he remains committed to client needs and nurturing his team.

Sources: With thanks to the Freight and Trade Alliance for their freight market update. Figures attributed to Drewry, Sea-Intelligence, WorldACD, UNCTAD and the Australian Bureau of Statistics as reported in the latest FTA/APSA Shipping Report.